Joint Accounts, Fixed Deposits, and Lockers: What the Law Really Says About Ownership After Death in India

For many Indian families, joint ownership of bank accounts, fixed deposits, and lockers is seen as a practical shortcut to ensure smooth transfer of assets after death. The belief is simple: if assets are held jointly—especially with an “either or survivor” clause—the surviving holder automatically becomes the owner.

However, a recent judgment of the Kerala High Court has once again clarified a critical legal principle that continues to be widely misunderstood:

Operational access is not the same as legal ownership.

This distinction lies at the heart of joint account after death India disputes, particularly in an era where estate planning is often informal or influenced by global templates that do not align with Indian law.

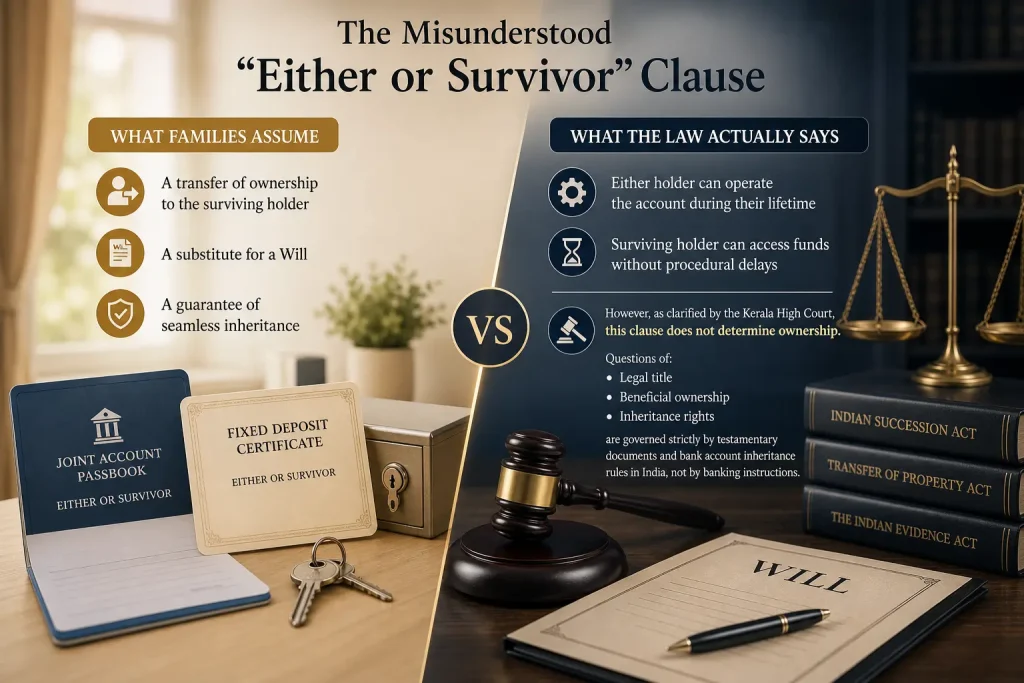

The Misunderstood “Either or Survivor” Clause

What Families Assume

Most joint banking arrangements in India—whether savings accounts, fixed deposits, or lockers—operate under an either or survivor clause in India.

For many families, this clause is interpreted as:

- A transfer of ownership to the surviving holder

• A substitute for a Will

• A guarantee of seamless inheritance

What the Law Actually Says

From a banking perspective, the either or survivor clause in India is designed for operational convenience. It allows:

- Either holder to operate the account during their lifetime

• The surviving holder to access funds after death without procedural delays

However, as clarified by the Kerala High Court, this clause does not determine ownership.

Questions of:

- Legal title

• Beneficial ownership

• Inheritance rights

are governed strictly by testamentary documents and bank account inheritance rules in India, not by banking instructions.

Joint Fixed Deposits: Access Does Not Mean Entitlement

The Legal Position

In the case of joint fixed deposits, Indian law draws a clear distinction between:

- Payment by the bank, and

• Entitlement to ownership

A surviving joint holder may legally withdraw the proceeds of a fixed deposit. Once the bank releases the funds, its obligation is fulfilled.

But Who Actually Owns the Money?

The critical point in joint account after death India scenarios is this:

- If a valid Will exists, the funds must be distributed according to that Will

• If there is no Will, the funds are governed by applicable succession laws

The surviving holder does not automatically become the owner. Instead, they effectively act as a custodian or trustee for the rightful heirs—similar to the legal position of a nominee.

This nuance is often overlooked and is one of the most common triggers of disputes under bank account inheritance rules in India.

Joint Bank Lockers: A More Complex Reality

Why Lockers Are Treated Differently

The Kerala High Court adopted an even more cautious approach when dealing with joint lockers.

Unlike bank accounts or deposits:

- A locker is merely a storage facility

• The bank has no knowledge of its contents

• Ownership of items inside is not verified

A locker may contain:

- Individually owned assets

• Jointly owned valuables

• Inherited property

• Assets belonging to third parties

The Court’s Position

The court clarified that:

- The principles applicable to joint accounts cannot be automatically applied to lockers

• Being a surviving locker holder does not confer ownership over its contents

In the case under consideration, a mother and daughter jointly held a locker. The mother had executed a registered Will, specifically bequeathing the gold ornaments inside to another family member.

Despite the daughter’s claim based on survivorship and alleged oral gifts, the court upheld the Will.

The outcome was clear:

The Will prevailed over the locker mandate.

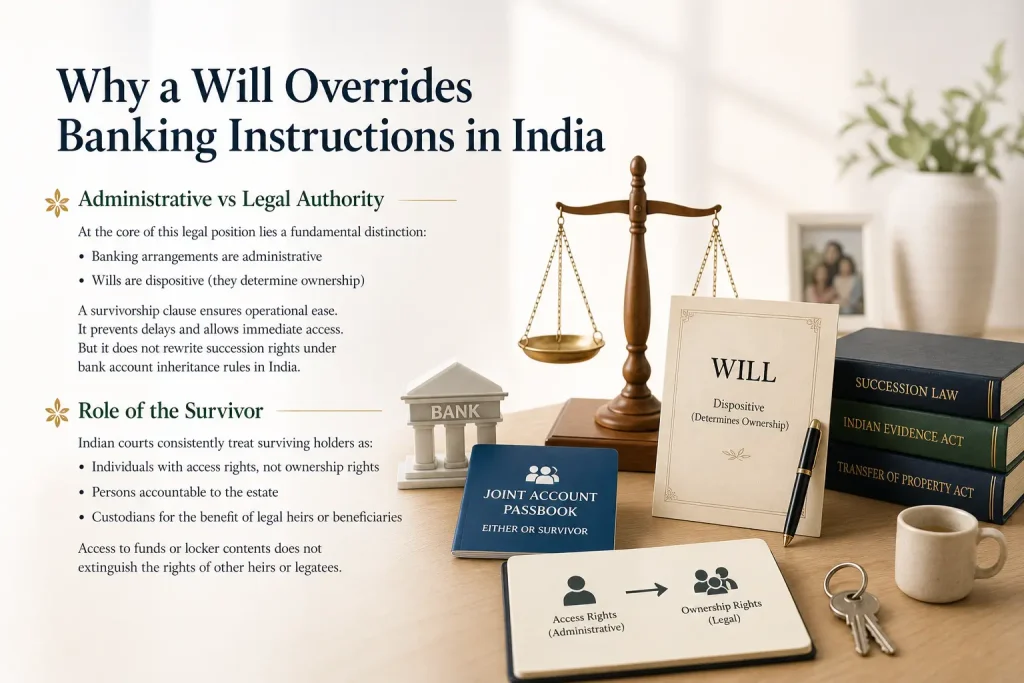

Why a Will Overrides Banking Instructions in India

Administrative vs Legal Authority

At the core of this legal position lies a fundamental distinction:

- Banking arrangements are administrative

• Wills are dispositive (they determine ownership)

A survivorship clause ensures operational ease. It prevents delays and allows immediate access. But it does not rewrite succession rights under bank account inheritance rules in India.

Role of the Survivor

Indian courts consistently treat surviving holders as:

- Individuals with access rights, not ownership rights

• Persons accountable to the estate

• Custodians for the benefit of legal heirs or beneficiaries

Access to funds or locker contents does not extinguish the rights of other heirs or legatees.

How the Western Position Differs

The U.S. Approach

In several Western jurisdictions, particularly the United States, the legal framework is fundamentally different.

Joint accounts are often held as:

- Joint tenants with right of survivorship

Under this system:

- Ownership automatically transfers to the surviving holder

• The asset bypasses probate

• The Will does not govern such assets

In fact, in many U.S. states, a properly structured survivorship clause or “payable on death” (POD) designation can override a Will.

Why This Creates Confusion in India

Many estate planning tools, templates, and AI platforms are heavily influenced by Western legal frameworks.

As a result, they often:

- Recommend survivorship-based planning

• Suggest structures that work in the U.S. or U.K.

• Fail to highlight that Indian law treats such arrangements differently

This creates a dangerous gap between perception and legal reality, especially in joint account after death India cases.

The Risk of Relying on Informal or Imported Planning

Where Things Go Wrong

Problems typically arise when individuals:

- Assume joint ownership equals inheritance

• Rely solely on banking mandates

• Use online templates not tailored to Indian law

• Avoid drafting a proper Will

The Consequence

This often leads to:

- Disputes among family members

• Legal claims against the surviving holder

• Delays in distribution of assets

• Emotional strain within families

What appears to be a simple arrangement can become a complex legal conflict under bank account inheritance rules in India.

Practical Takeaways for Families and Advisors

-

Joint Holding Is Not Estate Planning

Joint accounts, fixed deposits, and lockers are tools for convenience—not substitutes for succession planning, especially in joint account after death India scenarios.

-

A Will Remains Central

A properly drafted Will is the primary document that determines:

- Ownership of assets

• Distribution among heirs

• Intent of the individual

-

Survivors May Have Legal Obligations

Surviving joint holders must recognise that:

- Access does not equal ownership

• They may be accountable to other heirs

• Misuse of funds can lead to legal consequences

-

Avoid Blind Reliance on Templates

Estate planning should be tailored to:

- Indian legal frameworks

• Personal family structures

• Nature of assets

Imported templates or AI-generated documents must be used with caution, particularly when dealing with either or survivor clause India implications.

A Broader Perspective

This judgment reflects a consistent position taken by Indian courts:

Inheritance is governed by law, not by convenience.

While banking systems are designed to simplify operations, they cannot override the legal framework of succession.

Closing Thought

In an age where financial arrangements are becoming increasingly digitised and accessible, it is easy to mistake ease of access for clarity of ownership.

But estate planning does not operate on assumptions—it operates on documentation.

Joint accounts, fixed deposits, and lockers may help families manage assets during their lifetime. But when it comes to inheritance, the law looks beyond access and asks a more fundamental question:

Who did the owner intend to benefit?

In India, the answer to that question lies not in a banking clause, but in a carefully drafted Will—supported by a clear understanding of joint account after death India laws.

PlanMyEstate: Bringing Clarity to Ownership and Inheritance in India

At PlanMyEstate, we help families navigate the gap between banking convenience and legal ownership—a gap that often leads to disputes in joint account after death India scenarios.

Many individuals assume that joint holdings, nominee structures, or an either or survivor clause in India are sufficient for seamless inheritance. In reality, these are operational tools—not substitutes for legally valid estate planning.

Our approach focuses on aligning your financial arrangements with bank account inheritance rules in India and your true intent.

Our services include:

-

Will Drafting & Estate Structuring

Creating legally robust Wills that clearly define ownership, beneficiaries, and distribution—ensuring your intent prevails over default interpretations. -

Estate Plan Review

Identifying risks in existing arrangements such as joint accounts, fixed deposits, and lockers that may lead to disputes after death. -

Trust Planning & Implementation

Structuring private family trusts for better control, protection, and intergenerational wealth transfer. -

Succession Advisory

Ensuring your estate passes smoothly without litigation, confusion, or unintended outcomes. -

Asset Mapping & Ownership Clarity

Helping families clearly document who owns what—eliminating ambiguity between access and entitlement.

With the right planning, you can ensure that your assets are transferred not just efficiently—but correctly, legally, and without conflict.

People Also Ask (PAA) Optimized FAQs

-

Who owns a joint account after death in India?

In India, the surviving holder of a joint account does not automatically become the legal owner. Ownership is determined by the Will or succession laws, not by the joint account status.

-

What is the either or survivor clause in India?

The either or survivor clause allows the surviving account holder to access funds after death, but it does not grant ownership rights under Indian law.

-

Does a joint account override a Will in India?

No, a joint account does not override a Will. The distribution of assets is governed by the Will or applicable succession laws.

-

Can a nominee claim full ownership of a bank account in India?

No, a nominee is only a custodian of the funds. The actual ownership is determined by legal heirs or beneficiaries mentioned in the Will.

-

What are the bank account inheritance rules in India?

Bank account inheritance rules in India state that banks release funds to nominees or survivors for convenience, but legal ownership is decided by succession laws or a valid Will.

-

What happens to a fixed deposit after death in India?

A joint holder can withdraw the fixed deposit amount, but the funds must be distributed according to the Will or succession laws.

-

Who owns the contents of a bank locker after death?

The contents of a locker are not automatically owned by the surviving holder. Ownership depends on proof of ownership and the Will of the deceased.

-

Is joint ownership a substitute for estate planning in India?

No, joint ownership is not a substitute for estate planning. It only provides operational convenience and does not define legal ownership.

-

Can legal heirs challenge a surviving joint account holder?

Yes, legal heirs can claim their rightful share even if the surviving holder has withdrawn funds, as ownership is governed by succession laws.

-

How can you avoid disputes in joint account inheritance in India?

Disputes can be avoided by drafting a clear Will, reviewing estate structures, and ensuring alignment with Indian legal frameworks rather than relying only on joint holdings.

Take Control of What Happens Next

Don’t leave ownership to assumptions or banking shortcuts. Ensure your assets go exactly where you intend—legally, clearly, and without dispute. Create a properly structured Will and align your accounts today to protect your family tomorrow.